The world’s $900 trillion in real-world assets — real estate, commodities, bonds, private equity, art, infrastructure — has barely touched the blockchain. That is rapidly changing. RWA tokenization is the process of converting physical and traditional financial assets into programmable digital tokens on a blockchain, making them tradable, fractional, and accessible to a global pool of investors without the friction of traditional financial intermediaries.

In 2026, RWA tokenization is not an experiment confined to fintech whitepapers. BlackRock, Franklin Templeton, JPMorgan, Goldman Sachs, and UBS are all actively issuing and managing tokenized assets on public and permissioned blockchains. The tokenized asset market exceeded $15 billion in total value locked as of early 2026, with projections from Boston Consulting Group and major investment banks pointing to $16 trillion or more by 2030. This is a structural shift in how capital markets operate, not a passing trend.

This guide covers everything you need to understand about RWA tokenization in 2026: what it is, how the tokenization process works step by step, which asset classes are being tokenized, the measurable benefits, the real risks, case studies from institutional deployments, a detailed breakdown of the technology stack required to build a platform, and what the next five years looks like for this market. Whether you are an enterprise CFO exploring tokenization for your balance sheet, an investment manager looking to offer digital asset products, or a development team planning to build in this space, this is the comprehensive reference you need.

RWA tokenization is the process of creating a digital token on a blockchain that represents legal ownership of, or a defined economic claim on, a real-world asset. The token is implemented as a smart contract — a self-executing piece of code deployed on a blockchain — that encodes the terms of ownership, the rules governing transfer, dividend or income distribution logic, compliance requirements, and any governance rights attached to the asset.

The “real-world” in RWA is the critical distinction. Unlike Bitcoin or Ether — assets that exist purely on the blockchain with no external backing — an RWA token derives its value from something that exists in the physical or traditional financial world: a commercial building in Singapore, a US Treasury bond portfolio, a gold bar stored in a Swiss vault, a portfolio of trade finance invoices, or a share in a private equity fund. The token is a digital claim on that underlying asset, enforced by a combination of the smart contract code and the legal structure wrapping the asset.

Think of the token as the digital twin of a traditional financial instrument — a share certificate, a bond, a property title deed — but programmable, instantly transferable, infinitely divisible, and auditable by anyone at any time on a public ledger. The asset does not move or change when it is tokenized. The commercial building still stands. The Treasury bonds still mature. The gold still sits in its vault. What changes is how ownership is recorded, transferred, and managed.

The legal framework is as important as the technology. The token must map to a legally enforceable claim in the jurisdiction where the asset is located. This is typically achieved through a Special Purpose Vehicle (SPV) — a legal entity created specifically to hold the asset — whose shares or debt instruments are then tokenized. Token holders own a stake in or a claim on the SPV, and through it, on the underlying asset. This legal structure is what gives the token real-world enforceability beyond the blockchain.

A real-world asset (RWA) token is a blockchain-based digital representation of any asset that exists in the physical or traditional financial world, giving token holders legally enforceable ownership or economic rights backed by that asset.

RWA tokenization sits at the intersection of traditional finance (TradFi) and decentralised finance (DeFi). It brings the stability, scale, and legal certainty of traditional assets into the programmable, composable, globally-accessible world of blockchain — and it is creating an entirely new layer of financial infrastructure in the process.

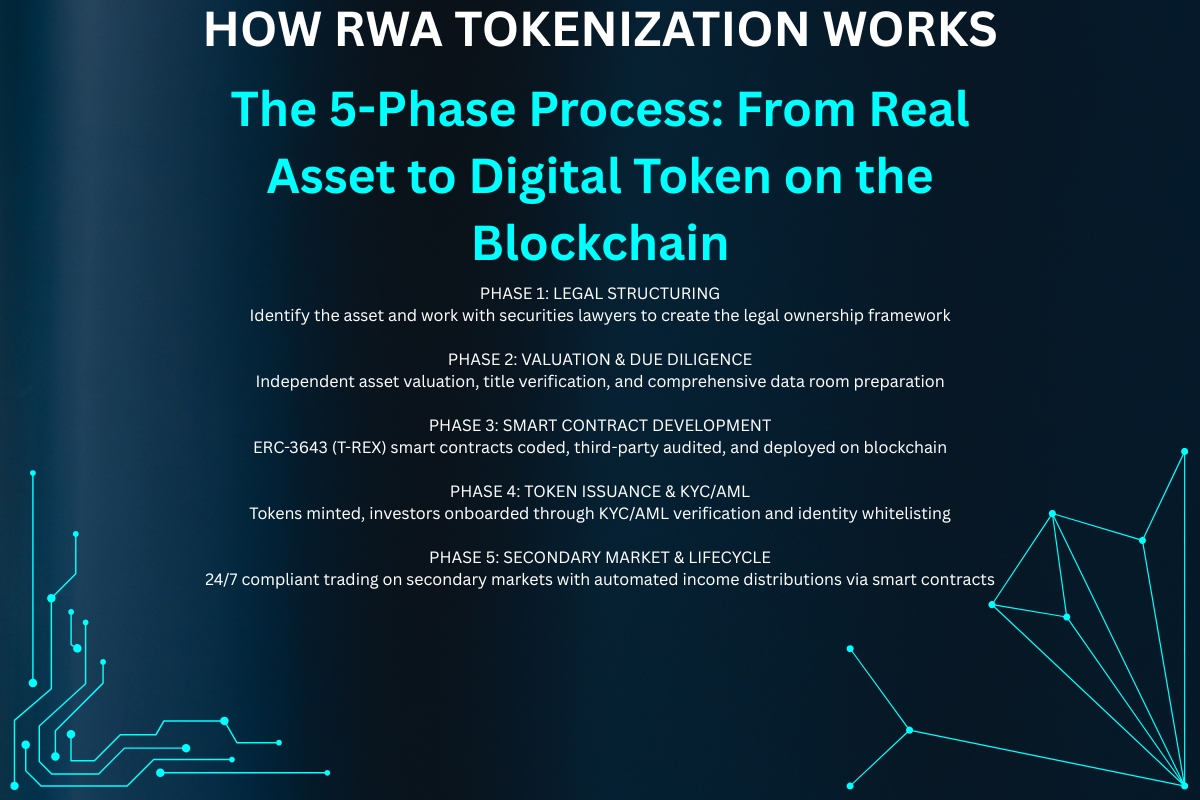

Tokenizing a real-world asset is a multi-disciplinary process involving legal counsel, financial structuring, blockchain development, compliance engineering, and ongoing asset management. It is not simply “putting an asset on the blockchain.” Here is a detailed breakdown of each phase:

The process begins with selecting an asset suitable for tokenization and structuring it correctly from a legal standpoint. Not every asset is straightforward to tokenize. The best candidates have a clear, legally enforceable ownership structure, a defined income stream or value basis, genuine investor demand for fractional or liquid access, and an underlying jurisdiction with a regulatory framework that accommodates digital securities.

The legal structuring phase involves working with securities lawyers and structuring advisors in the target jurisdiction to create the ownership vehicle. For most asset classes, this means establishing a Special Purpose Vehicle (SPV) — a company created solely to hold the asset. The SPV owns the building, the bond portfolio, or the commodity. The tokens then represent either equity shares in the SPV (giving holders ownership) or debt instruments issued by the SPV (giving holders a creditor claim and income stream).

Critically, this phase also defines what rights the token holders will receive: pure economic rights (dividends, rental income, coupon payments), governance voting rights (decisions on the underlying asset), or a combination. It establishes transfer restrictions — who can hold the token, what jurisdictions are eligible, what investor classification is required (accredited investor, institutional only, retail). These rights and restrictions are baked into the smart contract in the next phase, making them technically enforceable, not just contractually promised.

Before any tokens are issued, the underlying asset must be independently valued and documented. For real estate, this means a licensed property appraisal. For private equity or credit assets, it means audited financials and an independent valuation opinion. For commodities, it means assay reports and storage verification. This valuation sets the total token supply and the price per token. If a commercial building is valued at $10 million and you issue 10,000 tokens, each token represents $1,000 of asset value.

The due diligence phase involves compiling a comprehensive data room: title deeds, insurance policies, lease agreements, financial statements, environmental reports, legal opinions on the structure, and any regulatory filings required in the target jurisdiction. This documentation is increasingly stored on IPFS (the InterPlanetary File System) — a decentralised content-addressed storage system — so that the documentation linked to each token is permanently accessible and tamper-proof. Some platforms also use on-chain data attestation services like Chainlink Proof of Reserve to cryptographically verify the existence and value of the underlying asset on a continuous basis.

This phase is often underestimated by teams new to tokenization. Getting the legal and financial groundwork right takes longer than the technical development — typically three to six months for complex assets in regulated jurisdictions. Cutting corners here creates existential legal and regulatory risk for the entire project.

The smart contract is the technical core of the tokenization. It encodes everything: the total token supply, the token standard (ERC-20 for simple fungible tokens; ERC-3643 or ERC-1400 for compliance-heavy security tokens), the whitelist of eligible wallet addresses, transfer restrictions and their enforcement logic, income distribution calculations and distribution schedules, governance mechanisms, and the upgrade or redemption process for when the asset is sold or the SPV is wound down.

For security tokens with regulatory requirements, the ERC-3643 standard (also known as T-REX — Token for Regulated EXchanges) is the most widely adopted. It is an open standard maintained by Tokeny Solutions and used by major tokenization platforms including Société Générale’s Forge platform. ERC-3643 includes an on-chain identity registry that enforces KYC/AML compliance at the smart contract level — every transfer automatically checks whether both the sender and receiver are on the approved whitelist, and fails if they are not. This makes compliance programmable rather than procedural.

Before deployment, every production tokenization smart contract must go through a comprehensive third-party security audit by a reputable blockchain security firm — Trail of Bits, OpenZeppelin, CertiK, or Halborn. The audit checks for reentrancy vulnerabilities, access control flaws, integer overflow/underflow issues, logic errors in distribution or compliance mechanisms, and any deviations from the declared specification. Budget $15,000 to $60,000 for a thorough audit. This is not optional. Smart contract bugs are permanent and have resulted in hundreds of millions of dollars in losses across the DeFi ecosystem. No serious investor or institutional counterparty will engage with a tokenized asset whose contracts have not been independently audited.

Once smart contracts are audited, tested on a testnet, and approved for deployment, the token issuance process begins. This involves deploying the contracts to the mainnet, minting the initial token supply, and distributing tokens to initial investors. The distribution mechanism varies by asset class and regulatory framework: a private placement to accredited investors (most common for initial launches), a regulated public offering under securities law, or in some jurisdictions, a Regulation A+ offering open to retail investors.

Investor onboarding includes a KYC/AML verification process — collecting identity documents, verifying them against sanctions lists and PEP (Politically Exposed Person) databases, and recording the verified wallet address in the token’s identity registry. Major KYC providers used in tokenization include Jumio, Onfido, Synaps, and Fractal ID. These providers offer API-based identity verification embedded directly into the investor portal onboarding flow. The investor portal — a web application built on top of the smart contract — handles the complete investor experience: account creation, KYC submission, investment amount selection, payment (typically in stablecoins or fiat via a payment rail), and wallet-based token delivery.

Issuing a token does not automatically create liquidity. For tokenized assets to fulfil their promise of improved liquidity over traditional instruments, there must be a secondary market where token holders can sell to other eligible investors. This can be an existing regulated digital securities exchange (tZERO, Archax in the UK, INX, or Swiss Digital Exchange SIX SDX) or a custom-built secondary market module integrated into the issuer’s platform.

Secondary market infrastructure must enforce all the compliance checks from the primary issuance — a token can only transfer to a wallet that has passed KYC and meets the investor eligibility criteria. On ERC-3643 tokens, the smart contract handles this automatically on every transfer. Settlement is near-instant (seconds to minutes) compared to T+2 or T+3 in traditional markets, dramatically reducing counterparty risk and freeing up capital that would otherwise be trapped in settlement limbo.

Throughout the asset’s lifecycle, the smart contract handles all ongoing management automatically: distributing income (rental payments, bond coupons, dividend payments) directly to token holders’ wallets on the defined schedule, executing corporate actions (rights issues, buybacks), managing governance votes, and processing redemptions when the asset is sold or the fund winds down. This automated lifecycle management replaces manual processes traditionally handled by transfer agents, paying agents, and registrars — significantly reducing operational costs and eliminating human error from routine financial processes.

The tokenization market spans a remarkable range of asset classes in 2026, each at a different stage of technical maturity, regulatory acceptance, and market adoption:

| Asset Class | Adoption Stage | Key Examples |

|---|---|---|

| Real Estate | Early Mainstream | Fractional commercial and residential ownership, on-chain REITs, development project financing |

| Government & Corporate Bonds | Mainstream | BlackRock BUIDL, Franklin Templeton BENJI, tokenized corporate debt |

| Private Equity & Venture | Growing | Tokenized LP interests, secondary liquidity for private fund investors |

| Commodities | Growing | Gold tokens (PAX Gold, Tether Gold), oil and gas royalties, agricultural commodities |

| Private Credit & Trade Finance | Emerging | Tokenized invoices, letters of credit, supply chain financing instruments |

| Infrastructure | Emerging | Renewable energy assets, toll revenue streams, data centre ownership |

Tokenized Government Bonds and Money Market Instruments represent the most mature and highest-volume segment in 2026, driven by institutional demand for on-chain yield products. After DeFi’s native yields collapsed from their 2021 highs, crypto-native treasury managers and DeFi protocols needed stable, real-world yield sources. Tokenized US Treasuries offering 4–5% annual yield on-chain became immediately attractive. BlackRock’s BUIDL fund reached $500 million in assets under management within weeks of launch — the fastest AUM growth in money market fund history — validating institutional demand at scale.

Tokenized Real Estate is the category with perhaps the largest long-term opportunity. Global real estate represents an estimated $326 trillion in value, virtually all of it illiquid and accessible only to large investors or local buyers. Tokenization allows fractionalisation to as low as $50–$1,000 minimum investment, opens assets to global buyers across jurisdictions, and enables rental income to be distributed automatically in stablecoins on a weekly or monthly basis. The commercial real estate sector is following the residential model, with projects in Singapore, UAE, and the EU tokenizing office buildings, warehouses, and mixed-use developments.

Private Credit and Trade Finance are emerging categories where tokenization offers transformational liquidity improvements. Private credit — loans to mid-sized businesses that fall between bank lending and public bond markets — has traditionally been a 5–7 year illiquid investment locked in closed-end funds. Tokenization allows secondary market liquidity that was previously impossible. Trade finance instruments (invoices, letters of credit, receivables) are even shorter-dated — 30 to 180 days — and tokenization dramatically reduces the friction of originating, distributing, and settling these instruments globally.

The most visible benefit of RWA tokenization is fractionalisation — the ability to divide an asset into arbitrarily small units and distribute them to investors at any participation level. A commercial building in central London worth £50 million has traditionally been accessible only to institutional investors, REITs, or ultra-high-net-worth individuals with millions to deploy. Tokenize it into 500,000 tokens at £100 each, and suddenly a far broader range of investors can participate in premium real estate that was previously structurally unavailable to them.

This is not just about accessibility — it is about portfolio diversification. Retail and mass-affluent investors can now build diversified real asset portfolios across geographies, asset classes, and durations that previously required institutional capital. A teacher in India can hold a fractional stake in a Singapore office tower, a German logistics centre, and a US Treasury portfolio — all from a single wallet, all generating yield in stablecoins. This is a genuinely new capability that did not exist before tokenization.

For institutional investors, fractionalisation solves a different problem: the ability to deploy capital in exact sizes across a wider range of assets without being forced into large minimum ticket sizes. An endowment fund that wants $500,000 exposure to private credit across 10 different deals no longer needs to write $50,000 minimum checks to each fund — it can buy tokens on a secondary market with precise sizing and instant settlement.

Traditional real assets are notoriously illiquid. Selling a commercial building requires months of marketing, negotiation, legal work, and settlement. Private equity fund interests are typically locked for 7–10 years with no secondary market. Even listed REITs, while liquid, trade only during stock exchange hours and are accessible only to investors who can open brokerage accounts in the relevant jurisdiction.

Tokenized assets can trade on secondary markets 24 hours a day, 7 days a week, to any compliant buyer anywhere in the world. Settlement is near-instant — typically seconds to a few minutes on most blockchains — compared to T+2 or T+3 for traditional securities. The smart contract handles all compliance checks at the point of transfer, so there is no need for manual settlement intermediation.

This liquidity premium is financially significant. Academic research on illiquidity discounts in private markets consistently finds that investors demand a 2–5% annual premium to hold illiquid assets compared to equivalent liquid ones. If tokenization meaningfully improves secondary market liquidity for an asset class, it compresses that illiquidity discount — creating direct value for asset owners who can achieve higher valuations for their assets by making them more accessible and tradeable.

One of the most powerful but least-discussed benefits of tokenization is programmable compliance. With traditional securities, compliance is procedural — transfer agents check eligibility lists, brokers enforce selling restrictions, banks apply AML rules at the payment level. These checks are manual, expensive, slow, and error-prone. Compliance failures can lead to regulatory penalties and force unwinding of transactions that already settled.

With tokenized securities built on standards like ERC-3643, compliance is automatic and technically enforced at the smart contract level. The contract checks the KYC status, jurisdiction eligibility, and investor classification of both the sender and receiver on every transfer attempt. A transfer to an ineligible wallet simply fails — not because a human caught it after the fact, but because the contract mathematically cannot execute it. This makes compliance audit trails perfect and eliminates an entire class of procedural compliance failures.

Income distribution is equally transformed. Rental payments, bond coupons, loan interest, and dividend payments are executed automatically by the smart contract on the programmed schedule — with no manual payment processing, no delays caused by bank cut-off times, no disputes about payment amounts. A property token that distributes monthly rental income sends the proportional amount directly to every token holder’s wallet simultaneously, globally, in seconds. The cost of distributing income to 10,000 token holders is essentially the same as distributing to 10.

Every transaction involving a tokenized asset — every ownership transfer, every income distribution, every governance vote, every compliance update — is recorded on the blockchain. This creates a permanent, immutable, publicly auditable ledger of the complete history of the asset’s token ownership and operations.

For asset managers, this dramatically simplifies audit and regulatory reporting. Instead of maintaining complex internal ledgers and reconciling them with custodians, transfer agents, and paying agents, the blockchain provides a single source of truth that all parties can verify independently. Regulatory reporting becomes a matter of querying the on-chain data rather than aggregating information from multiple internal systems and counterparties — cutting compliance overhead significantly.

For investors, full transparency means they can verify their holdings, their income history, and the complete transaction history of their tokens at any time without relying on a custodian’s statement. This eliminates a systemic trust requirement that has historically been a source of fraud risk in alternative asset markets — from misreported returns to outright ownership fraud.

The intermediary chain in traditional asset transfers is long and expensive. Buying a commercial property involves estate agents, lawyers, surveyors, transfer agents, settlement banks, and potentially custodians — each taking a fee. Even secondary market bond transfers involve broker commissions, clearing fees, and settlement costs. The total frictional cost of transferring ownership of a traditional real asset typically runs to 3–10% of transaction value.

Smart contract-based tokenization compresses this dramatically. The contract handles transfer, settlement, and compliance verification automatically. The only costs are the blockchain network gas fee (typically $1–$50 on Ethereum L1, fractions of a cent on Polygon or other L2s) and the platform fee charged by the tokenization provider. Industry analysis by the World Economic Forum and Boston Consulting Group projects that tokenization can reduce transaction costs by 40–80% across major asset classes compared to traditional transfer mechanisms — representing hundreds of billions of dollars in annual cost savings at full market scale.

The benefits of RWA tokenization are compelling, but the challenges are equally real. Any business or investor approaching this space with clear eyes needs to understand and plan for these risks:

Securities laws vary dramatically by jurisdiction, and what constitutes a legally compliant tokenized security in Switzerland may trigger violations in the United States, Singapore, or the UAE. Most tokenized assets that carry economic rights — ownership stakes, revenue claims, debt repayment rights — are classified as securities in the jurisdictions where they are offered or sold. This subjects them to full securities regulation: prospectus requirements, investor eligibility restrictions, marketing restrictions, and ongoing disclosure obligations.

There is no global harmonised framework for digital securities. The EU’s MiCA regulation provides a framework for crypto assets but explicitly excludes MiFID II financial instruments, which most RWA tokens qualify as — those remain governed by existing securities law. The UK’s FCA has a separate framework. The US SEC’s approach has been evolving through enforcement action rather than clear guidance. Singapore’s MAS has been one of the most proactive jurisdictions, providing regulatory sandboxes and clear guidance through Project Guardian. For any tokenization project targeting investors across multiple jurisdictions, legal counsel in each target market is non-negotiable.

Smart contracts are immutable once deployed — which is both their strength (the rules cannot be changed without governance approval) and their risk (a bug cannot be patched with a simple software update). The history of DeFi is filled with examples of smart contract exploits that resulted in hundreds of millions of dollars in losses: the DAO hack in 2016, the Ronin bridge hack, the Euler Finance exploit. Many of these exploits took advantage of subtle logical errors in contract code that passed basic testing but were discovered by sophisticated attackers probing edge cases.

For RWA tokenization, where the contracts control access to real-world asset cash flows and ownership rights, the stakes are even higher. A bug in the income distribution logic could result in incorrect payments. A flaw in the transfer restriction logic could allow tokens to be transferred to ineligible wallets, triggering regulatory violations. An access control vulnerability could allow an attacker to mint unlimited tokens, diluting existing holders. Comprehensive third-party audits are mandatory — and even post-audit, upgradeability mechanisms and emergency pause functions should be built into the contract architecture as a backstop against unforeseen issues.

Many tokenized asset use cases depend on external data being brought on-chain: the current market value of a property, the rental income received in a given month, compliance flags from KYC providers. This data is delivered by oracles — off-chain services that feed information into smart contracts. Oracle failure or manipulation is a material risk. If an oracle reports incorrect income data, the smart contract distributes incorrect amounts. If a price oracle is manipulated, it can trigger incorrect liquidations or redemptions.

Chainlink is the dominant institutional-grade oracle network and is used by the majority of serious tokenization platforms. Its decentralised node network and data aggregation approach significantly reduce single-point-of-failure risk. Chainlink’s Proof of Reserve product continuously verifies that the claimed underlying asset exists and has the stated value — a critical safeguard for assets like tokenized commodities or real estate. But no oracle system is perfectly immune to data integrity issues, and tokenization platforms must design their systems to handle oracle failures gracefully with circuit breakers and fallback mechanisms.

Issuing a token does not create a liquid secondary market. For smaller token issuances — a single building, a small credit fund — there may not be enough natural buyer-seller flow to create genuine secondary market liquidity without active market-making. Illiquid secondary markets defeat one of the core value propositions of tokenization. Building genuine secondary market liquidity requires a strategy from day one: partnering with existing regulated secondary market venues, seeding market maker relationships, structuring the token issuance to ensure a wide enough initial investor base, and potentially designing automated market making pools for more liquid token types.

The institutional adoption of RWA tokenization moved from pilot to production between 2023 and 2025, with several landmark products now operating at meaningful scale:

BlackRock launched the BUIDL fund on the Ethereum blockchain in March 2024 in partnership with Securitize. BUIDL invests in US Treasury bills, repo agreements, and cash equivalents — effectively a money market fund, but issued as an ERC-20 token on Ethereum. It reached $500 million in assets under management within weeks, demonstrating institutional appetite for on-chain money market instruments at a scale that surprised even optimistic observers. The fund pays daily accrued yield to token holders, distributed as new BUIDL tokens, with redemption into USDC available through Circle’s on-chain infrastructure. BUIDL has since become one of the primary forms of high-quality collateral used within the DeFi ecosystem.

Franklin Templeton’s BENJI fund, launched initially on Stellar and subsequently expanded to Polygon, was one of the first SEC-registered tokenized fund products. Crucially, it uses the blockchain as the official record of share ownership — not a parallel system alongside a traditional register, but the actual fund register. BENJI tokens represent shares in an SEC-registered money market fund investing in US government securities. The fund crossed $400 million in AUM and demonstrated that a traditional asset manager could operate a fully compliant, blockchain-native fund product within the existing US regulatory framework — a landmark proof point for the entire industry.

Ondo Finance built tokenized access to US Treasury yield for DeFi users globally — specifically targeting investors in jurisdictions that cannot easily access US interest-bearing accounts directly. USDY (Ondo US Dollar Yield) is a tokenized note backed by US Treasuries and bank demand deposits, available to non-US persons. OUSG provides institutional-grade tokenized Treasury exposure. Ondo’s innovation is making traditional Treasury yield accessible and composable within the DeFi ecosystem — USDY is used as collateral in DeFi lending protocols and as liquidity in DEX pools, bringing real yield into on-chain financial applications.

Maple Finance built a protocol for institutional on-chain credit — effectively a marketplace for tokenized corporate loans. Borrowers apply for credit, undergo a credit assessment process run by specialist pool delegates, and receive funding from on-chain liquidity providers who hold tokenized loan positions. Maple has originated over $2.5 billion in on-chain loans and represents a significant proof point for private credit tokenization, demonstrating that risk underwriting, loan structuring, and debt servicing can all be managed effectively using blockchain infrastructure at meaningful institutional scale.

RealT has tokenized over 400 US residential properties and made them available to global investors via Ethereum. Each property is held in an LLC; the LLC membership interests are tokenized using ERC-20 on Ethereum. Investors receive weekly rental income distributions in DAI (a decentralised stablecoin) automatically via the smart contract. Minimum investments are as low as $50 per token. RealT is one of the longest-running real estate tokenization platforms and has proven the operational viability of the model across hundreds of properties and thousands of global investors over multiple years.

Building a production-ready RWA tokenization platform is a significant engineering and legal undertaking. The platform must simultaneously be technically robust, legally compliant, operationally scalable, and commercially viable. Here is a component-by-component breakdown of what is involved:

The first architectural decision is which blockchain to deploy on and which token standard to use. Ethereum is the most established platform for security tokens. The largest institutional tokenization deployments — BUIDL, BENJI, Ondo, RealT, Maple — are all Ethereum-based. The security token standard ecosystem (ERC-3643, ERC-1400) is most mature on Ethereum. Polygon (Ethereum-compatible Layer 2) offers dramatically lower gas costs — typically $0.001–$0.10 per transaction versus $1–$50 on Ethereum L1 — with full Ethereum tooling compatibility. Avalanche is popular for institutional tokenization because of its customisable subnet architecture. Solana offers very high throughput and very low fees, making it attractive for high-volume applications like trade finance or mass-market retail tokenization.

For a regulatory-compliant security token platform, the ERC-3643 standard (T-REX) is the recommended foundation. It provides an on-chain identity registry tracking verified wallet addresses, a compliance module encoding transfer rules, and the token contract itself. The compliance module can be configured to enforce jurisdiction-based restrictions, investor classification checks, maximum investor counts, lock-up periods, and any other transfer condition your legal structure requires. Beyond the token contract, you need contracts for income distribution, governance (if token holders have voting rights), redemption (for token buybacks or fund liquidation), and upgradeability using proxy patterns that allow contract logic updates without full redeployment.

| Component | What It Involves | Key Technology |

|---|---|---|

| Token Contract | Core token logic, supply, transfer rules | ERC-3643 / ERC-1400 on Ethereum or Polygon |

| Identity Registry | On-chain whitelist of KYC-verified investors | ERC-3643 OnchainID |

| Compliance Module | Transfer restriction enforcement logic | Custom Solidity, ERC-3643 framework |

| Distribution Engine | Automated income distribution to holders | Custom contract + Chainlink Automation |

| KYC/AML Integration | Investor identity verification and whitelist management | Jumio, Onfido, Synaps, Fractal ID via API |

| Oracle Integration | Real-world data feeds for pricing and compliance | Chainlink Price Feeds + Proof of Reserve |

| Investor Portal | Full-stack web app for onboarding, purchase, portfolio management | React + ethers.js / wagmi, Web3Modal |

| Secondary Market | Compliant trading venue or integration with existing DSE | Custom order book or integration with tZERO, Archax |

| Admin Dashboard | Issuer tools for distributions, reporting, compliance management | Custom React admin panel |

| Security Audit | Third-party code review before mainnet deployment | Trail of Bits, OpenZeppelin, CertiK, Halborn |

The blockchain choice matters significantly. Ethereum is the most established for security tokens but carries higher gas costs. Polygon offers lower gas costs with Ethereum-compatible tooling. Avalanche subnets are popular for banks and regulated institutions that need a permissioned environment while maintaining Avalanche’s security. The right chain depends on your asset class, expected transaction volume, regulatory constraints, and the DeFi ecosystem you want your token to be composable with.

A basic RWA tokenization platform — covering smart contract development, KYC integration, an investor portal with wallet connectivity, and a comprehensive security audit — typically costs between $80,000 and $250,000 to build from scratch with an experienced blockchain development team. This assumes a single asset class, a single blockchain, and a relatively straightforward legal structure.

Enterprise-grade platforms with multi-asset support, multiple blockchain deployments, secondary market functionality, oracle integration, institutional-grade custody integration, and full regulatory compliance infrastructure across multiple jurisdictions cost $500,000 to $2,000,000 or more for initial development. Development timelines range from 3–4 months for a focused MVP to 9–12 months for a full enterprise platform. Plan for ongoing annual operational costs of 15–25% of initial build cost for maintenance, security updates, audit refreshes as contracts are upgraded, and compliance monitoring.

The trajectory for RWA tokenization is unambiguously upward. Market size projections are striking: Boston Consulting Group projects $16 trillion in tokenized assets by 2030. Standard Chartered and PwC analyses suggest similar figures. Even the more conservative Bank for International Settlements (BIS) estimate points to trillions in tokenized financial assets by the end of the decade. The base case for 2026–2027 is continued institutional-led growth in tokenized money market instruments and bonds, followed by accelerating real estate and private credit tokenization as legal and operational infrastructure matures.

Regulatory convergence will be the biggest accelerant. As more jurisdictions pass clear digital asset securities frameworks — following the EU’s MiCA, Singapore’s MAS guidelines, and the UK’s FCA digital asset roadmap — the legal certainty required by institutional issuers will be established. The US remains the largest unresolved question: the absence of clear guidance for tokenized fund products is holding back the full scale of US institutional participation. When that clarity arrives, it will catalyse a significant step-change in US tokenized asset issuance.

DeFi composability will be transformative for RWA economics. As tokenized real-world assets become accepted as high-quality collateral in major DeFi lending protocols — Aave, Compound, MakerDAO, and their successors — asset owners gain access to on-chain capital that was previously only available to crypto-native assets. A tokenized bond portfolio that can be used to borrow USDC on Aave effectively becomes liquid in a new way, enabling capital efficiency that traditional bond holders cannot access. This composability premium will drive significant institutional interest in maintaining tokenized versions of their asset portfolios.

Cross-chain interoperability is the remaining infrastructure challenge. Today’s tokenized asset ecosystem is fragmented across multiple blockchains with limited portability between them. Cross-chain bridge protocols and interoperability standards like CCIP (Chainlink’s Cross-Chain Interoperability Protocol) are developing the infrastructure to make tokenized assets genuinely portable across blockchains — a prerequisite for a unified global tokenized asset market where investors can seamlessly move between ecosystems.

Businesses that build their tokenization infrastructure now — while competition is still limited and experienced blockchain talent is available — will have a significant first-mover advantage as mainstream adoption accelerates through 2027 and beyond. The window is open, but it is closing.

Yes, in most major jurisdictions — but the legal structure and compliance framework are what make it legal. Tokenized assets that confer ownership rights, economic rights, or debt claims on real-world assets are typically classified as securities under the laws of most developed markets. This means they must be issued through a properly structured, legally compliant offering and marketed only to eligible investors in eligible jurisdictions.

The key is working with qualified securities lawyers in each target jurisdiction from the earliest stage of structuring. Attempting to bypass securities law by framing a tokenized security as a utility token is a high-risk approach that has led to significant regulatory enforcement actions. Structure it correctly from the start — the additional legal cost upfront is far less than the cost of a regulatory enforcement action later.

There is no universal answer — the right blockchain depends on your asset class, target investor base, transaction volume, regulatory constraints, and DeFi composability goals. Ethereum is the most established for institutional security tokens due to its mature ecosystem, proven security, and deep DeFi composability. Polygon is preferred for cost-sensitive applications and retail-facing products. Avalanche subnets suit banks and regulated institutions needing a permissioned environment. Solana works for high-throughput, low-cost use cases.

The practical advice: if maximum DeFi composability and the deepest institutional infrastructure are your priority, build on Ethereum and optionally expand to Polygon for cost efficiency. If you are a bank needing a permissioned environment, evaluate Avalanche subnets. If cost and throughput are paramount, consider Solana or Polygon. Many production platforms are now multi-chain — starting on one chain and bridging to others as cross-chain infrastructure matures.

A basic platform covering smart contract development, KYC integration, an investor portal, and a security audit typically costs $80,000–$250,000 for a single asset class on a single blockchain. Enterprise-grade multi-asset, multi-chain platforms with full regulatory compliance infrastructure cost $500,000–$2,000,000+. Ongoing annual operational costs typically run 15–25% of initial build cost. Budget separately for legal structuring ($50,000–$200,000+ depending on jurisdiction and asset complexity) and regulatory counsel in each target market.

Both involve blockchain tokens, but they are fundamentally different instruments. An NFT (Non-Fungible Token) represents a unique digital item — artwork, a collectible, a game asset. Each NFT is one-of-a-kind and non-interchangeable. NFTs are generally not regulated as securities. An RWA token typically represents fractional ownership of or economic rights in a real-world asset — a building, a bond, a commodity. Most RWA tokens are fungible (every token is identical and interchangeable, like shares of stock) and are regulated as securities. The use cases, regulatory treatment, technical standards, and market infrastructure are distinct.

Building a tokenization platform from scratch takes 3–6 months for a focused development team. Tokenizing a specific asset — legal structuring of the SPV, due diligence, valuation, regulatory filings, smart contract deployment, and investor onboarding — typically takes 2–4 months for a straightforward asset in a jurisdiction with clear digital asset regulation. Complex assets in jurisdictions requiring full prospectus-level disclosure can take 6–12 months. The legal and regulatory work, not the technical development, is almost always the long pole in the tent.

Web4Next specialises in blockchain and Web3 development for enterprise clients entering the digital asset and tokenization space. We have built tokenization infrastructure across multiple blockchains and asset classes — from ERC-3643 security token smart contracts and comprehensive security audits to full-stack investor portals, oracle integrations, and secondary market modules.

Our team combines deep blockchain engineering expertise with a practical understanding of the regulatory and legal dimensions of tokenized assets — because a tokenization platform that does not work legally is not a platform at all.

If you are exploring RWA tokenization for your business — whether you are at the “should we do this?” stage or ready to begin architecture design — we are ready to have that conversation. Contact Web4Next for a free 30-minute technical consultation, or explore our Blockchain Development services and DeFi Development services for more on what we build.

Nikhil Khandelwal